For most of the industry's history, insurance has had one type of customer: a person, a business, or a government entity trying to protect something of value from an uncertain future. The underlying transaction has remained largely unchanged since Edward Lloyd opened his coffeehouse in the seventeenth century. A party with exposure transfers a portion of that risk to an entity structured to hold it. The form has evolved. The participants have not.

That is changing faster than most of the industry has noticed.

AI agents are not a speculative technology. They are operating right now — executing trades, managing supply chains, provisioning cloud infrastructure, negotiating procurement contracts on behalf of the organizations that deploy them. As their autonomy and scope expand, they will manage cargo logistics, extend credit, source energy, and enter binding commercial agreements at machine speed and machine scale. They will, in short, become economic actors with real exposure to uncertain outcomes.

Economic actors with real exposure to uncertain outcomes need insurance. The question worth asking — and the one the industry has been slow to grapple with — is whether the infrastructure exists to provide it.

The honest answer today is no. Not because the will isn't there, but because three structural mismatches make existing insurance architecture incompatible with the agent economy.

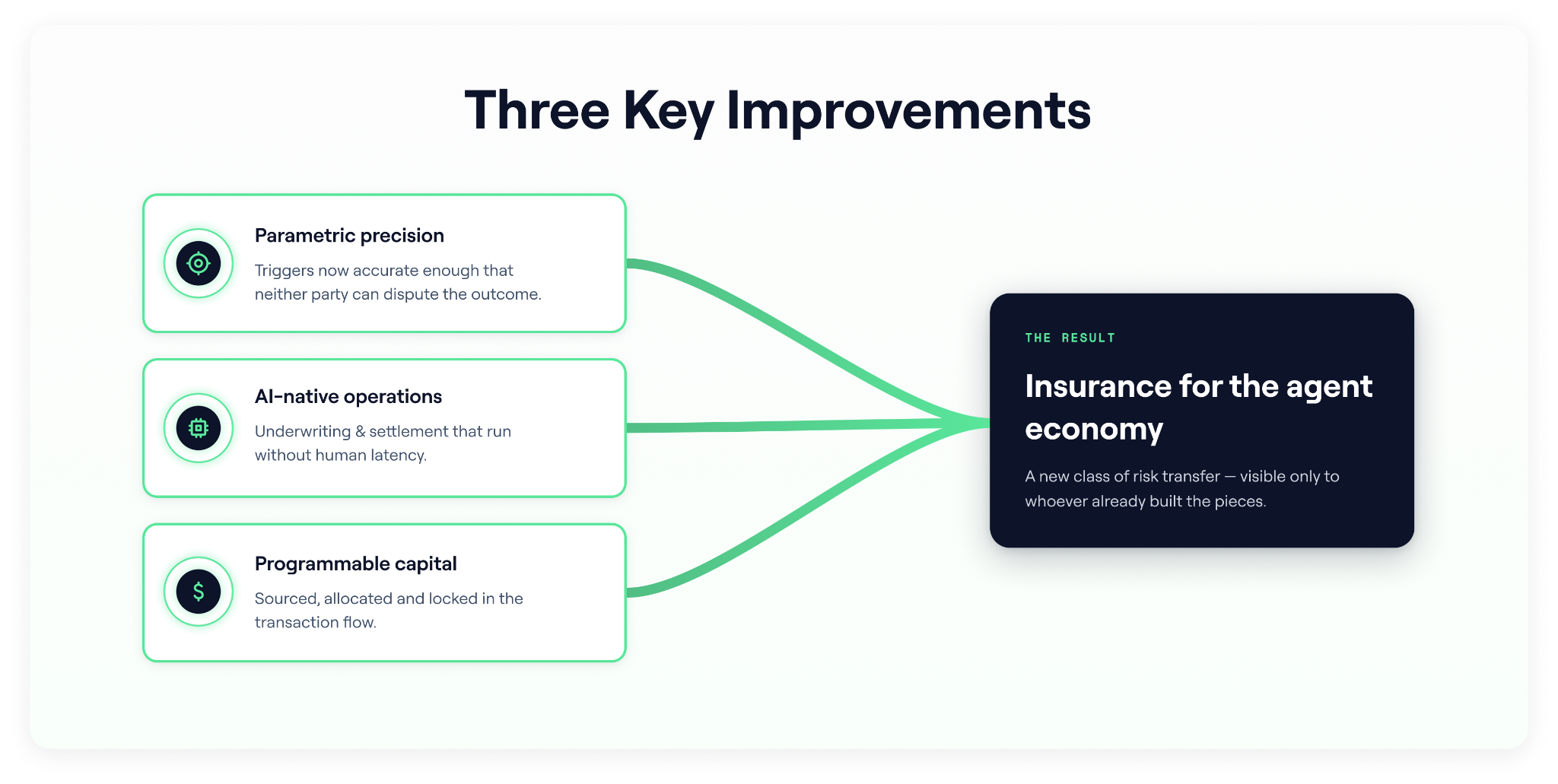

The first is speed. Traditional insurance is built around human timelines. A claim requires documentation, investigation, adjudication, and settlement — processes measured in weeks and months. An AI agent transacting at machine speed cannot wait for an adjuster. The coverage structure that works for autonomous systems is parametric: triggered by objective, verifiable data at the moment a specified condition is met, with settlement that follows automatically. This is not a new concept in insurance. What is new is the precision required. Parametric coverage for AI agents only works when the trigger model is accurate enough that neither party can reasonably dispute the outcome. Building that level of precision has historically been the hard part.

The second mismatch is operational architecture. If the insured is an AI system operating at scale — potentially managing thousands of transactions simultaneously — the insurer cannot be a human organization operating at human speed. Underwriting, pricing, and settlement all need to function as software: continuously updated, capable of operating at the transaction volumes that machine-speed commerce generates, integrated directly into the systems the agents use. An insurer that receives a submission, routes it to an underwriter, and responds in 48 hours is not a viable counterparty for an autonomous system making real-time decisions.

The third mismatch is capital structure. Binding coverage at machine speed requires capital that can be sourced, allocated, and locked programmatically. The economic terms of a parametric policy need to live in a form that can be verified and executed in the same transaction flow as the underlying commercial activity — not in a PDF sitting in someone's inbox waiting for a counter-signature.

These are not incremental problems. They represent a category of risk that the existing insurance infrastructure was not designed to serve. But they are also, viewed from a different angle, a significant opportunity. The agent economy will generate risk transfer demand at a scale and frequency that no existing market can fully absorb. The carriers and structures that build for it now will be positioned as the infrastructure layer for an entirely new class of economic activity.

What makes this moment particularly interesting is the convergence happening beneath it. The precision required to make parametric triggers trustworthy has improved dramatically as AI-native risk models have matured. The operational architecture required to underwrite at machine speed exists now in ways it did not five years ago. The capital structures needed to settle in real time are further along than most insurance practitioners realize. None of these developments was specifically aimed at the agent economy. Each was driven by other pressures. Their convergence is what creates something genuinely new.

History suggests this is how the most significant technological leaps actually happen — not from a single breakthrough, but from multiple independent developments reaching sufficient maturity simultaneously. Clocks from gears and springs. Telescopes from glass-making. The printing press from screw mechanisms, oil-based ink, and movable type. In each case, the convergence produced something that looked obvious in retrospect and was almost invisible in prospect.

The AI agent economy presents insurance with a version of that moment. The participants best positioned to recognize it are not necessarily the largest carriers. They are the ones that have already built the infrastructure components the moment requires: parametric structures precise enough to be trusted by both parties, AI-native operational architecture that can underwrite and settle without human latency, and capital structures designed for programmable deployment. The challenge for the industry is recognizing that the next customer is arriving before the infrastructure built to serve them is finished — and moving accordingly.

The alternative — waiting for the agent economy to fully materialize before building — is likely to produce the same result it always has when incumbent industries wait too long to engage with a structural shift. Not extinction, but permanent displacement from the most valuable part of what comes next.