In the past, the word “uninsurable” was mostly used in theory, a remote edge case for rare catastrophes or hypothetical systemic risk. But today, “uninsurable” is showing up in policyholder letters and regulator testimony. In states like Florida, California, and Hawaii, the term is no longer abstract. It’s showing up in real time, in the form of cancelled policies, withdrawn carriers, and skyrocketing premiums.

At its core, the idea of insurance depends on being able to price and pool risk. When that becomes impossible, due to frequent, severe, or unpredictable events, insurance markets break down. What we’re witnessing now isn’t just a failure of pricing. It’s a systemic failure of insurance infrastructure to keep pace with climate volatility, and a growing gap between the needs of vulnerable communities and the risk appetite of capital providers.

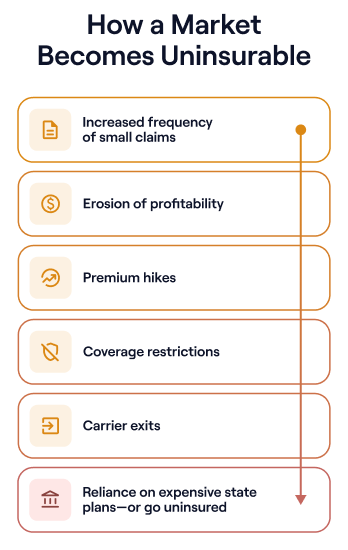

The Crisis Isn’t Just “Big Storms” — It’s a Thousand Smaller Cuts

Much of the media narrative around insurance collapse centers on large, high-impact disasters: wildfires leveling entire towns, hurricanes carving paths through the Gulf, or floods submerging highways. These are certainly part of the picture, and they’ve driven billions in losses. But what’s making many markets uninsurable isn’t just the headline-grabbing megastorms. It’s what the industry calls attritional loss: small, chronic claims that accumulate year after year and erode carrier profitability.

In California, it’s a pattern of seasonal wildfires and claims inflation. In Hawaii, it's compounding fire and flood risk. In Louisiana and Florida, it's not just hurricanes, it's mold claims, roof repairs, and litigation that collectively make underwriting unprofitable, even in years without a major storm.

The result is a creeping erosion of insurance availability. Carriers raise rates. Then restrict coverage. Then stop writing new policies. Eventually, they pull out altogether. Homeowners and businesses are left with two options: turn to expensive last-resort state plans, or go uninsured.

Recent data illustrates this trend. According to the National Association of Insurance Commissioners, average homeowners' premiums in Florida rose over 40% from 2020 to 2023. In some counties, the increases exceeded 100%. In Hawaii, insurers have scaled back coverage after devastating wildfires in 2023 led to unprecedented property losses. And in California, major carriers like State Farm and Allstate have stopped writing new homeowners policies altogether. In each case, the exits are not due to one catastrophic event, but to an accumulation of climate-related pressure points.

Why Traditional Insurance Can’t Keep Up

This unraveling has less to do with poor modeling or bad business decisions, and more to do with structural limitations in how insurance and reinsurance are set up today. Most carriers operate under strict solvency and capital adequacy requirements. These frameworks weren’t built for the scale and frequency of climate volatility we’re now seeing.

Many carriers also rely on historical loss data to set premiums, data that is quickly losing relevance in a warming world. Even with modern catastrophe models, pricing can’t always move fast enough to reflect reality. Regulatory approval cycles, consumer protection rules, and competitive pressures keep rates from adjusting to match rising risk. Meanwhile, claims continue to come in.

On the capital side, reinsurers — who backstop most property insurance portfolios — are also under strain. After several years of elevated catastrophe losses, many have raised prices, restricted terms, or exited certain regions. This makes it harder for carriers to secure affordable reinsurance, further compounding the withdrawal from high-risk areas.

This squeeze on both sides, underwriting losses and capital retreat, is what ultimately makes a market uninsurable.

Rethinking the Model: Parametric Coverage + Intelligent Capital

If the traditional system is struggling to keep up, what’s the alternative? At Arbol, we believe the path forward lies in reimagining both how coverage is structured and how capital is deployed.

That starts with parametric insurance. Unlike traditional indemnity policies, which pay out based on assessed damages, parametric policies trigger payouts based on objective, pre-defined conditions, like wind speed, rainfall, or temperature. This allows for faster, more transparent claims and removes the need for time-consuming inspections and documentation. Critically, it also reduces loss adjustment expense (LAE), which is one of the major cost drivers in volatile markets.

Parametric insurance isn't new, but it's becoming more viable and scalable thanks to better data, improved modeling, and broader capital support. At Arbol, we’ve built a full-stack parametric platform that uses AI underwriting, satellite data + in-house peril specific models, and dynamic pricing to structure efficient, scalable coverage for climate-exposed markets.

But product innovation isn’t enough on its own. What often gets overlooked in the conversation about “uninsurable” markets is the role of capital. Even the best-structured coverage doesn’t matter if there’s no capacity to support it.

That’s why Arbol has also focused on building a capital strategy alongside our product infrastructure. We work with global reinsurers and institutional investors to create climate-linked investment vehicles, including parametric reinsurance and insurance-linked securities (ILS), that match capital to risk more efficiently. These instruments offer clear, rules-based payout structures and uncorrelated return potential, making them attractive even in high-volatility regions.

When you pair efficient, tech-enabled underwriting with flexible, diversified capital, you get a system that can function where traditional insurance fails.

Toward a More Resilient Insurance Infrastructure

What’s needed now isn’t just a new product or a better premium. It’s an entirely new infrastructure for pricing, distributing, and backing climate risk. That includes:

- Coverage models that reflect real-time conditions, not historical norms

- Capital frameworks that align investor incentives with climate resilience

- Technology that reduces administrative overhead and accelerates response time

- A willingness to step into markets others have left behind, but with a better system, not just more risk

Arbol’s approach is built around this vision. And while there’s no single fix to a challenge as complex as climate-driven uninsurability, we believe this integrated model, combining product, technology, and capital, is a meaningful step forward.

If you’re interested in how we’re applying this approach in markets like Florida and Hawaii, check out the latest episode of This Way Forward, where Arbol CEO Sid Jha shares the story behind our decision to enter markets others were leaving — and what it takes to build resilience from the ground up.