When most people think of climate insurance, they imagine a single farmer protecting their crop from drought or hail. But the reality of climate risk is far broader. A failed harvest or supply disruption doesn't stop at the farm gate, it ripples across entire supply chains, impacting processors, exporters, retailers, and lenders alike. As climate volatility accelerates, the need for more flexible, scalable insurance solutions is becoming urgent, not just for producers, but for the full web of actors who depend on them.

This is where embedded parametric insurance is gaining traction. Instead of offering standalone policies that require complex underwriting and slow claims processes, embedded insurance is integrated directly into existing business systems and financial flows. For agriculture and other climate-exposed sectors, this shift is creating entirely new ways to manage risk, from seed to shelf.

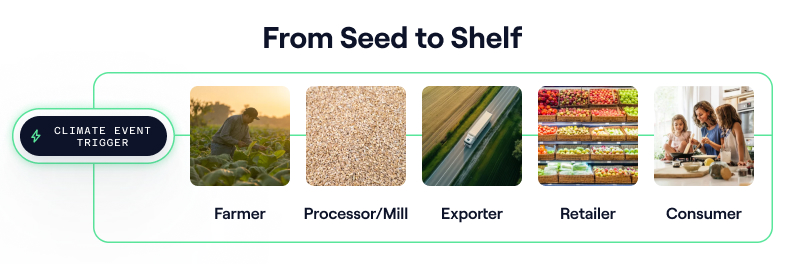

Climate Risk Is a Supply Chain Problem

Climate shocks affect entire value chains. A drought doesn’t just reduce a farmer’s yield, it can idle a mill, disrupt a co-op’s exports, or strain a processor’s ability to meet contracts. When extreme heat reduces power output at a solar plant, the financial strain cascades from the plant owner to the utility to the grid operator. In fisheries, port closures due to cyclones or rough seas can delay processing, reduce income for boat crews, and trigger missed delivery deadlines for global buyers.

Yet in many of these sectors, traditional insurance simply doesn’t reach the full set of participants. The barriers are well-documented:

- Small or informal actors are underinsured, if insured at all.

- Coverage is often restricted to physical loss, not operational or income disruption.

- Manual claims and high administrative costs limit the viability of low-value or decentralized policies.

According to the World Bank, less than 20% of agricultural producers in developing economies have access to any formal insurance — and even fewer supply chain participants are protected downstream.

Parametric Insurance Enables Scale

Parametric insurance offers a fundamentally different model. Instead of paying claims based on an assessment of physical damage, parametric policies pay out when measurable, pre-agreed thresholds are triggered. This could be rainfall below a certain level, temperatures above a threshold, or a port closure index driven by satellite or sensor data.

Because they rely on objective, third-party data and don’t require field inspections, parametric products are faster, more transparent, and less expensive to administer. They’re also highly adaptable, able to cover risk in sectors and geographies where traditional insurers either can’t or won’t go.

For supply chains, this unlocks new opportunities to embed climate protection into existing relationships, financial products, and contracts. For example:

- A co-op can offer drought protection to all member farmers during seed sales.

- A lender can embed rainfall coverage into seasonal working capital loans.

- A commodity buyer can build delay-triggered payouts into off-take agreements with exporters.

- A fishing company can offer weather-indexed downtime protection to boat crews.

The key is that coverage becomes part of the transaction — not a separate, hard-to-access process.

Embedding Insurance Also Requires Embedding Capital

Product innovation alone isn’t enough. To truly scale embedded insurance across supply chains, capital must also be part of the equation. Many insurance gaps today aren’t just about product limitations, they stem from the lack of risk capacity in the system. Insurers often pull out of volatile regions not because they lack ideas, but because they can’t secure affordable reinsurance or investment support.

That’s why capital innovation is as important as product design in solving climate insurance challenges.

At Arbol, we address this through our integrated capital model. We work with global reinsurers and institutional investors to back our parametric insurance products with flexible, diversified capital — including reinsurance treaties, collateralized layers, and insurance-linked securities (ILS). This capital enables us to:

- Support large-scale programs across entire producer networks or industries.

- Offer consistent pricing and capacity, even in high-risk regions.

- Provide liquidity for rapid payouts following climate-triggered events.

This alignment of product and capital allows us to serve actors across the supply chain, from smallholder farms to global trading desks, without relying on traditional indemnity assumptions or underwriting constraints.

Arbol in Action: Supply Chain Resilience by Design

Arbol’s embedded model is already active across multiple sectors:

- Agriculture: We partner with AG platforms, input distributors, and cooperatives to offer rainfall, heat, and soil moisture protection directly through digital ordering systems and mobile agents.

- Renewables: We help energy providers hedge solar or wind underperformance, embedding parametric triggers into financial agreements and project-level contracts.

- Fisheries: Our coastal weather index products provide income protection to fishers facing port closures or rough seas — coverage that’s embedded into fleet financing or insurance platforms.

- Finance and Lending: We support banks and microfinance institutions by embedding coverage into credit products, reducing loan defaults tied to extreme weather.

In each case, the goal is not just to offer insurance — but to integrate it into the systems and financial flows that people already use.

The Benefits of Embedding Climate Insurance

Embedding climate protection across supply chains isn’t just about convenience — it has real-world impacts:

- Improved financial inclusion for producers and workers historically left out of formal insurance systems.

- Faster recovery from weather shocks, thanks to automated payouts.

- Stronger creditworthiness and loan repayment rates, reducing systemic risk for lenders.

- Greater commercial stability, as businesses gain confidence in the continuity of supply and revenue.

Perhaps most importantly, embedded insurance fosters resilience by design, turning every transaction, contract, or purchase into an opportunity to reduce climate risk.

Looking Ahead

As climate disruptions become more frequent and interconnected, the question is no longer whether to insure supply chains, but how. Parametric insurance, when embedded into the financial and operational fabric of climate-exposed sectors, offers a scalable, efficient, and forward-looking answer.

At Arbol, we’re building the infrastructure to make this possible, from the underwriting models to the capital structures, and from the APIs to the policy triggers. The future of climate resilience doesn’t live in isolated insurance policies. It lives in every shipment, every loan, and every transaction that keeps a supply chain moving.

If you’re interested in learning how embedded climate insurance can strengthen your supply chain, reach out to our team or explore our upcoming case studies.