Every major carrier in the United States has announced an AI strategy in the past three years. Chief AI officers have been hired. Vendor partnerships signed. Conference panels are oversubscribed. Industry spending on AI is growing more than 25% this year alone.

A March 2026 analysis drawing on data from McKinsey, EY, Deloitte, and Swiss Re gave this moment a name: "Pilot Purgatory." Most of the industry is spending heavily on AI and getting almost nothing back. The reason is not a lack of tools. It is a lack of architecture.

Arbol was founded in 2018 on a different premise entirely — not that AI could improve insurance, but that insurance needed to be rebuilt from scratch with intelligence as the load-bearing structure. We started in parametric agriculture, the most data-intensive and least forgiving corner of the market, where a model that cannot accurately predict crop yields produces coverage that does not actually protect anyone. There was no legacy architecture to retrofit because we built nothing that required it. The data infrastructure, the risk models, the underwriting logic, the claims workflows, and the actuarial engine were designed together, from the beginning, as a unified system.

Seven years later, that architecture is producing documented results at Lilypad, our admitted property and casualty carrier operating across nine coastal states. The numbers are specific enough to be worth examining in detail.

Underwriting: from queue to decision in seconds

In a traditional carrier, a residential submission enters a queue. An underwriter reviews it against a checklist applied through a rules engine built for a previous era of risk. The quote is assembled and issued over hours or days. Industry research puts 70 to 80 cents of every insurance IT dollar toward maintaining these systems, leaving almost nothing for building anything new.

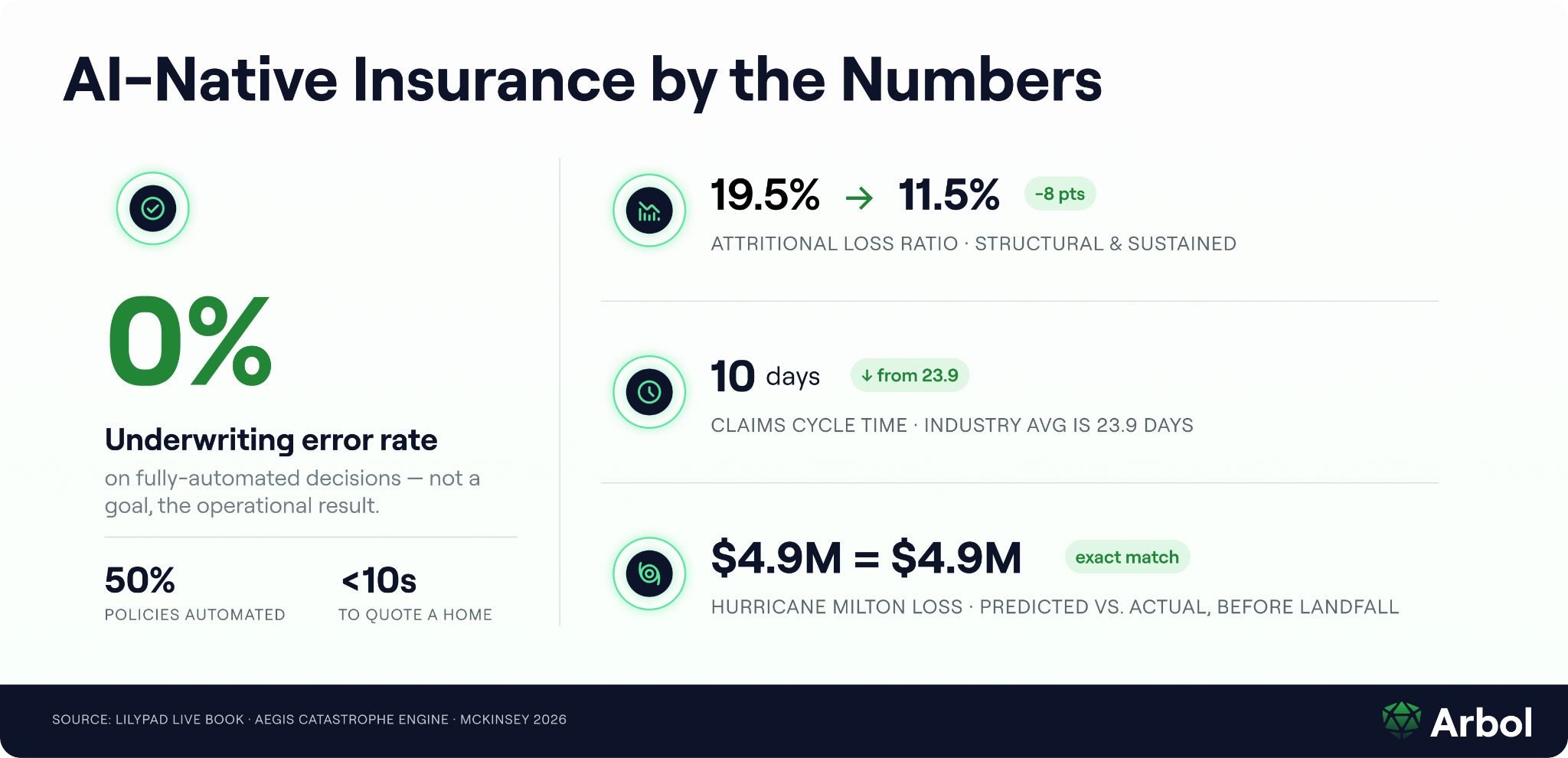

At Lilypad, the residential underwriting process runs through SmartWrite, an AI agent drawing on the same proprietary data infrastructure powering our catastrophe models. Fifty percent of policies are now fully automated. Residential quotes return in under ten seconds. The error rate on automated decisions is zero.

Zero is not a goal. It is the operational result of a system designed to recognize the boundaries of its own confidence. Submissions that fall outside the automated tier route to underwriters with a complete analytical brief already prepared — exposure profile, comparable risks, relevant loss history, recommended range. The underwriter makes a judgment call on a fully structured case, not a blank submission.

Lilypad's attritional loss ratio dropped from 19.5% before AI underwriting was deployed to 11.5% afterward — an 8 percentage point structural improvement across the entire book, sustained across market cycles. The expense ratio, currently running approximately 20% consolidated against a regional carrier peer average of 25 to 30%, will reach 10 to 15% as remaining automation milestones complete. At that point, premiums can double without adding a dollar of fixed cost. Growth becomes operationally free.

Claims: building capacity the industry couldn't previously afford

A standard property claim involves nineteen discrete steps. From first notice of loss to closure, the process consumes between 100 and 120 minutes of adjuster and staff time per file. According to J.D. Power's 2024 U.S. Property Claims Satisfaction Study, the average claims cycle time has risen to 23.9 days under normal conditions and 34.2 days for catastrophe-related claims — six days longer than two years prior, as severe weather volume has strained an already fragile system. Customer satisfaction has fallen to its lowest level in seven years as a direct result.

For most carriers, claims volume is a cost problem with no clean solution. More claims means more adjusters. More adjusters means more overhead. The ceiling is structural.

That ceiling is what Lilypad's claims AI is designed to remove — not by cutting capacity, but by expanding it. Every step in the claims process was mapped against a single question: does this step require human judgment, or does it require human time? Human judgment — evaluating a coverage dispute, managing a policyholder through a traumatic loss, assessing a contested estimate — is irreplaceable. Human time spent on data entry, document classification, letter generation, and routing produces no better outcome than a system built specifically to handle it.

Seven of the nineteen steps now run fully automated: acknowledgment letters, coverage notes, intake records, structured data extraction, document classification, adjuster routing, and closure notifications. Those steps save 26 minutes per claim. Three additional steps operate as AI-assist workflows — reading the independent adjuster report, comparing third-party estimates against internal figures, and line-item reconciliation — saving a further 45 minutes per file. Six more steps are on the active roadmap, each designed through the same lens: what does the regulatory framework require, and how does AI help the adjuster meet that requirement with more precision, not less?

The reconciliation workflow shows what this produces in practice. When a third-party public adjuster or contractor submits an estimate, the traditional process requires two hours of manual review to find discrepancies and prepare for negotiation. The AI-assist reconciliation tool ingests the external estimate, generates a structured line-by-line comparison against the internal figure, and flags every divergence — in under 15 minutes. In a recent live claim, the internal estimate was $7,800 across 54 line items. The third-party submission came in at $46,500 across 164 line items — a $38,700 gap — with every divergent line surfaced before the adjuster entered the conversation. Lilypad runs approximately 20 such claims per week through this workflow. In a CAT event, that same infrastructure handles volume spikes without emergency staffing.

None of this operates outside regulatory view. The Claims Audit AI Agent runs Lilypad's mandatory biannual MA compliance audits — a process that previously required a full internal team and external contractors for a week — at 12 to 15 minutes per file. The Q1 audit processed 72 files. The audit trail is more complete, more consistent, and faster to produce than the manual process it replaced. AI has not created a compliance shortcut. It has created compliance infrastructure that never falls behind regardless of volume.

The result is a claims operation that handles materially more at a higher service level without proportional cost growth. Adjusters focus on the cases that require judgment because the system has already handled everything that doesn't. When CAT events hit multiple states simultaneously, the automated tiers absorb the surge. Regulators get more auditable decisions. Policyholders get faster resolutions. The business gets something the rest of the industry cannot easily replicate: the ability to grow premium without the overhead penalty that has always defined what growth in insurance costs.

Actuarial: continuous model rather than annual cycle

The traditional actuarial function operates on a review cycle. Data accumulates, models update, pricing adjusts for the following period. In coastal property markets where hurricane intensification is accelerating, and in wildfire-exposed regions where fuel loads and suppression dynamics have changed fundamentally, that lag is a structural pricing error compounding year over year.

Arbol's actuarial AI closes that loop in real time. The Aegis engine — our proprietary catastrophe model covering fourteen perils built in partnership with dClimate — refreshes as frequently as hourly. Every policy written feeds back into the calibration dataset. Loss experience is incorporated continuously, not at the next scheduled review.

The model's accuracy is validated by live events, not backtests. During Hurricane Category 5 Milton in October 2024, Aegis calculated a $4.9 million expected loss on Lilypad's exposed portfolio before the storm made landfall. The actual loss was $4.9 million — an exact match against real capital at risk. This is not a calibration exercise. It reflects seven years of live trigger-outcome records — every parametric policy written, every trigger evaluated, every actual loss recorded — feeding a closed loop that vendor models built on public data and updated on vendor timelines cannot replicate regardless of how they are marketed.

The wildfire actuarial infrastructure runs 20,000 years of stochastic synthetic fire perimeters to produce return-period loss estimates at parcel resolution. Built in-house, by the same team underwriting the risk, continuously updated with new vegetation, fuel load, and suppression data. Lloyd's reviewed it and approved Arbol for wildfire parametric underwriting — an institutional vetting process that no software tool alone passes.

For agricultural risks, the actuarial model produces county-level crop yield forecasts months before USDA publishes official figures, at less than 3% error against actuals. This is the data foundation Arbol has been building since 2018 — not because an AI moment arrived and demanded it, but because parametric coverage that cannot accurately predict outcomes is not insurance. It is a financial instrument that transfers uncertainty without reducing it.

What this means for the industry

McKinsey's analysis finds that early AI leaders in insurance are generating roughly six times the total shareholder returns of their laggard peers — and the gap is compounding. The carriers that built the architecture are pulling away from those that bought the tools.

The industry's instinct is to frame AI as a cost story — fewer people doing the same work. That framing misses what is actually available. The right frame is capacity: the same people handling more, with greater consistency, inside a regulatory structure that is fully met at every step. Lilypad can deliver exceptional service and grow premium substantially without adding a dollar of overhead.

A carrier that automates one step in an underwriting workflow has a faster process. A carrier that rebuilds underwriting as an AI agent workflow has an 8-point better loss ratio and a zero percent error rate. A carrier that deploys a claims chatbot has a marginally better NPS score. A carrier that rebuilds claims as an intelligence-first operation cuts cycle time from 23.9 days to 10, passes mandatory compliance audits in minutes rather than weeks, and handles CAT volume without standing up an emergency response. A carrier that licenses a vendor cat model gets a periodic update. A carrier that runs its own continuously calibrated model calls Hurricane Milton to the dollar.

That is not the result of an AI strategy announced in 2023. It is the result of an architecture built in 2018, when no one was calling this an AI moment, because the problem demanded it regardless of what anyone was calling it.