If you own a home within twenty miles of the coast, you've probably opened a letter from your insurance company in the past year that made your stomach drop. Maybe it was a cancellation notice. Maybe it was a renewal premium that doubled overnight. Or maybe it was a new policy with a deductible so high you wondered what you're even paying for.

You're not alone. Coastal homeowners across the United States are facing an insurance crisis that's fundamentally changing what it means to own property near the water.

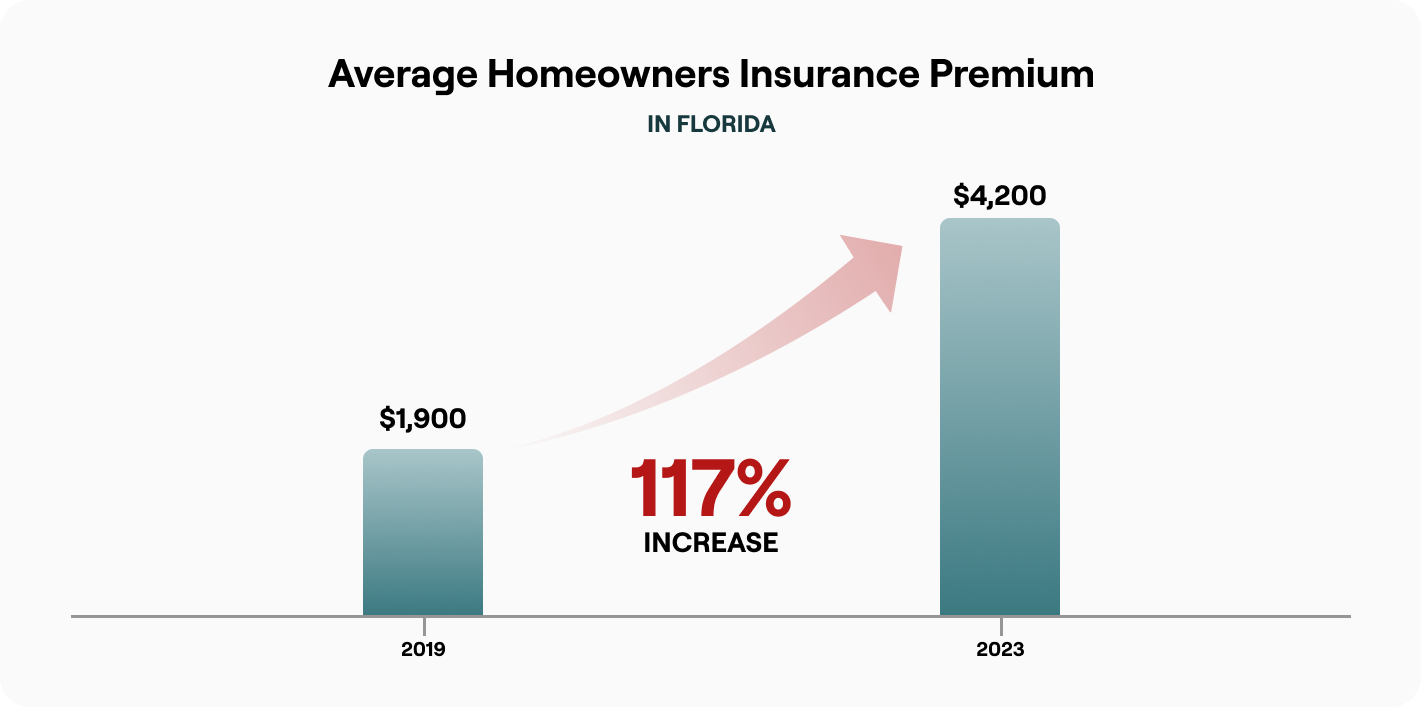

The Numbers Tell a Stark Story

Between 2018 and 2023, major insurers pulled out of coastal markets at an accelerating pace. State Farm stopped writing new policies in California. Farmers Insurance withdrew from Florida entirely, dropping 100,000 policyholders. Allstate followed suit in both states, along with parts of Louisiana and North Carolina.

The result? In Florida alone, the average homeowners insurance premium jumped from $1,900 in 2019 to $4,200 in 2023. That's a 117% increase in four years. Some coastal homeowners now pay more for insurance annually than they do for property taxes.

These aren't temporary market fluctuations. They represent a fundamental shift in how insurers view coastal risk.

What Changed?

Three factors converged to create this crisis, and they're not going away.

Climate patterns shifted in ways that invalidated decades of actuarial models. Hurricane frequency didn't increase dramatically, but intensity did. A Category 1 hurricane used to be a manageable risk. Now, storms rapidly intensify from tropical depressions to Category 4 monsters in 24 hours, giving coastal communities almost no time to prepare.

When Hurricane Ian hit Florida in 2022, it caused $112 billion in damage. That single storm wiped out years of insurance company profits. Insurers aren't just responding to that one event—they're looking at the trend line and seeing storms that were once "100-year events" happening every few years.

Reinsurance costs exploded. Most people don't know this, but insurance companies buy coverage too. It's called reinsurance, and it's how they spread risk globally. When coastal losses mounted, reinsurers dramatically increased their rates or pulled out entirely. This forced primary insurers to either raise premiums to cover the higher reinsurance costs or exit the market.

The Domino Effect on Homeowners

When major insurers leave, homeowners don't just face higher premiums. The entire structure of homeownership becomes unstable.

You can't get a mortgage without insurance. Banks require proof of coverage before closing. As traditional insurers exit, homeowners are forced into state-backed insurers of last resort. In Florida, Citizens Property Insurance Corporation—the state's insurer of last resort—now covers 1.3 million policies, triple what it held five years ago. These policies cost more and often provide less coverage.

Home values become unpredictable. When insurance costs $8,000 a year instead of $2,000, buyers factor that into their offers. Some markets are seeing 15-20% discounts on coastal properties that would have sold at a premium a decade ago. If you're planning to sell in the next few years, rising insurance costs are already eating into your equity.

Why Traditional Solutions Aren't Working

State regulators are trying to help. Some states capped rate increases or mandated that insurers can't drop policyholders without cause. These regulations seem consumer-friendly, but they often backfire.

When regulators block rate increases that insurers say they need to remain solvent, insurers simply stop writing new policies in that state. It's not about greed—it's about not wanting to operate at a loss. The result is fewer options for homeowners, not more.

State insurance programs were designed as safety nets for a small percentage of high-risk properties. They were never meant to insure millions of homes. As these programs grow beyond their intended capacity, they become financially unstable. If a major hurricane hits and the state program can't pay all claims, taxpayers end up covering the shortfall.

What This Means for Your Property

If you currently own coastal property, you're facing decisions that seemed unthinkable a decade ago.

Retrofitting has become essential, not optional. Impact-resistant windows, reinforced roofs, and hurricane shutters used to be nice-to-haves. Now, they're requirements for getting any coverage at all. Insurers are offering discounts for these upgrades, but you need to spend $20,000 to $50,000 upfront to qualify. Some homeowners are finding that even after retrofitting, their premiums still increase.

A Different Approach to Coastal Risk

Traditional insurance companies are retreating from coastal markets because their century-old model can't adapt fast enough to changing climate patterns. Lilypad-Centauri takes a fundamentally different approach. Instead of relying on historical data that no longer predicts future risk, we use AI data modeling tied to actual weather measurements—things like wind speed, rainfall, and storm surge height measured by satellites and weather stations.

AI is fundamentally changing how we predict weather and understand climate patterns. Traditional weather models run physics equations through supercomputers, taking hours to produce forecasts. AI models trained on decades of satellite data and weather observations can now generate accurate 10-day forecasts in minutes. For climate modeling, AI identifies patterns in massive datasets that humans would miss—like how specific ocean temperature changes six months ago predict hurricane intensity today. This speed and precision means better risk assessment, faster disaster warnings, and more accurate insurance pricing for weather-dependent coverage.

At Lilypad-Centauri, we're working directly with coastal communities, insurance agents, and homeowners to build coverage that actually makes sense for the risks you're facing—not the risks actuaries modeled in 1985.

The Bigger Picture

This isn't just a coastal problem anymore. Wildfire risk is creating similar dynamics in California, Colorado, and Oregon. Tornado risk is reshaping insurance in the Midwest. Flood risk from inland storms is affecting properties nowhere near the coast.

What's happening to coastal homeowners is a preview of what's coming to other high-risk areas. Insurance companies are getting better at identifying risk and pricing it accurately—or refusing to take it on at all.

The insurance crisis exposes a fundamental tension: we built millions of homes in places that are becoming increasingly risky to insure, and traditional insurance companies don't have good systems in place for dealing with that reality.